Mortgage Broker vs Bank in UAE: Which Should You Choose?

Securing a mortgage is one of the most consequential financial decisions you will make in the UAE. Yet many buyers give little thought to how they arrange it, defaulting to whichever route their property agent happens to suggest. That decision quietly shapes how much you pay, how quickly you are approved, and how much of your own time the process consumes.

The choice usually comes down to two paths: going directly to a bank, or working through a mortgage broker. Both can deliver a mortgage. They do not deliver the same experience. This guide breaks down the real differences so you can choose with clarity rather than by default.

First, what stays the same either way

Before comparing the two routes, it helps to understand what does not change regardless of which you choose.

-

The underlying lending rules are identical across routes. The UAE Central Bank caps LTV, the Debt Burden Ratio, and the loan tenor for every lender.

-

Headline rates tend to be similar for the same buyer profile, because banks publish standard rate cards and competition has compressed the spread.

-

The mortgage rate quoted should be the same regardless of which broker you use, since banks do not pad rates to compensate for broker commissions.

So the difference is not the rules. It is service, access, and the bank's best available pricing.

Going direct to a bank

For some buyers, especially those with an existing banking relationship, the direct route makes sense.

The advantages:

-

It is the cheapest route in absolute terms, with zero broker fee, and it can be fast if you already bank with the lender.

-

Transferring your salary account to the mortgage bank can unlock relationship pricing discounts of 0.1 to 0.25%, which banks like Emirates NBD, ADCB, and FAB actively incentivise.

-

A long-standing relationship can occasionally smooth approval where the bank already knows your financial history.

The limitations:

-

You see only one bank's offer and you handle the entire process yourself.

-

Applying directly can be a slow exercise in bureaucracy, with banks heightening risk-assessment protocols, leading to longer processing times and more paperwork for the average applicant.

-

A single error in your application carries real risk. A mistake can lead to a rejection that stays on your AECB credit bureau record for months.

In short: lowest absolute cost, but a single viewpoint and all the legwork on your shoulders.

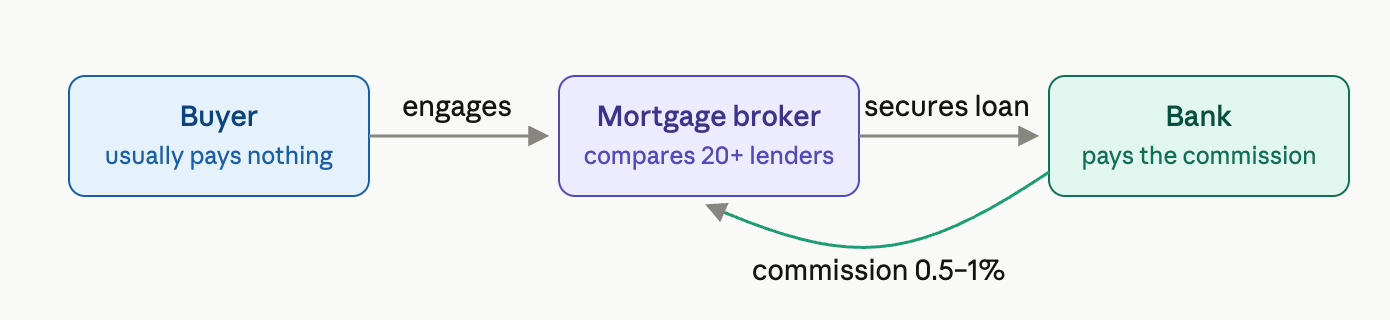

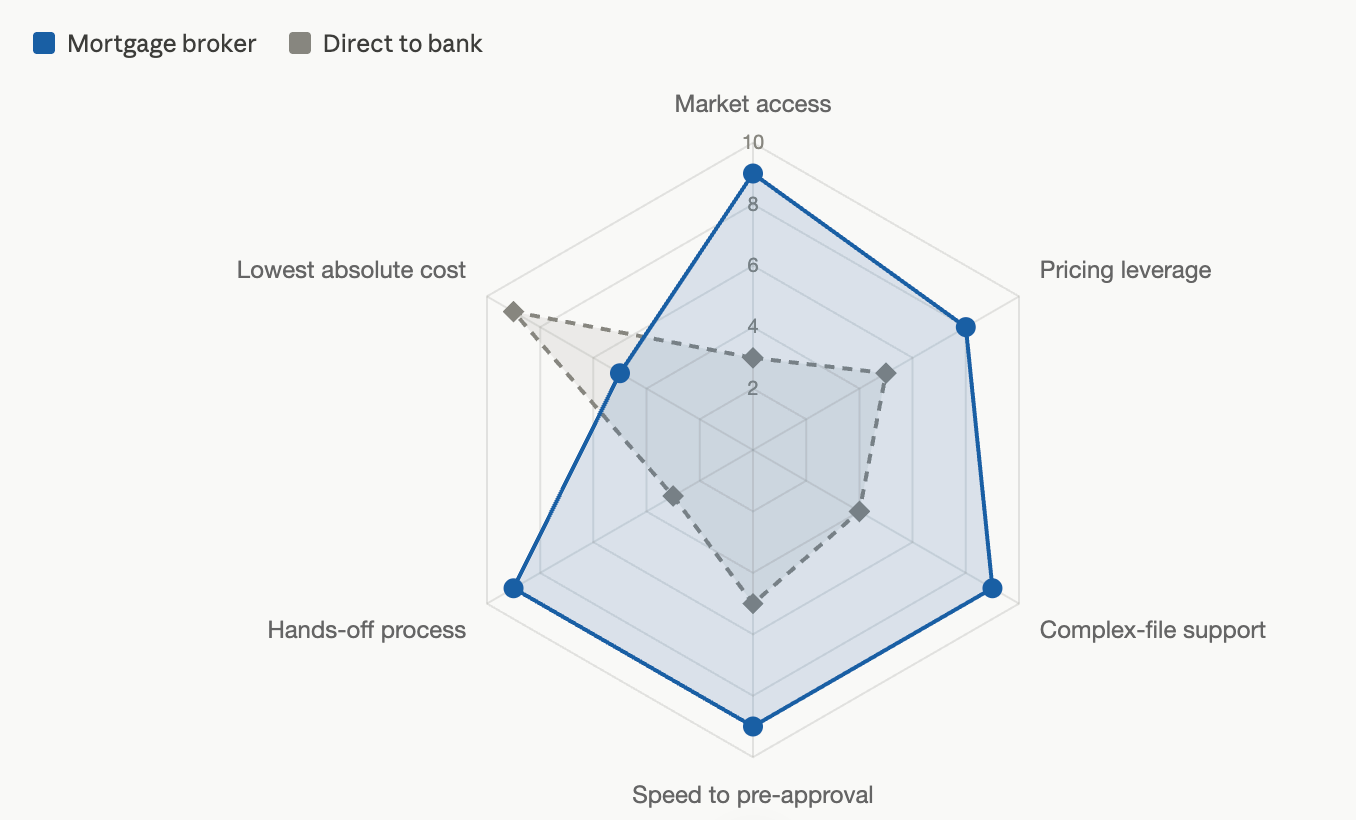

Working through a mortgage broker

A mortgage broker sits between you and the lenders, comparing the market on your behalf and managing the application end to end.

The advantages:

-

Whole-of-market access. A strong broker navigates the internal appetites of 20 or more lenders, knowing which banks are over-exposed to certain sectors and which are looking to grow their mortgage books aggressively.

-

Genuinely better pricing in practice. While headline rates are similar, the actual rate you receive can vary by 0.10 to 0.30% depending on negotiation strength and the channel you came through.

-

Usually free to the buyer. Brokers typically earn commission from the bank, around 0.5 to 1% of the loan, so most clients pay nothing.

-

Specialist help for complex files. First-time buyers, the self-employed, those with foreign income, and non-residents are the clearest candidates for a broker.

-

A real edge for non-residents. Only four to six UAE banks lend to non-residents, each with specific documentation requirements, so a broker specialising in these files is almost always worth it.

-

Speed that strengthens your negotiating position. A fast pre-approval gives you a cash-buyer advantage, and a quick closing can be traded for a 5 to 8% discount on the asking price.

-

They manage the full journey. A broker analyses your income and goals, presents a best-in-market comparison of bank offers, leverages relationships for approval, and coordinates valuation and DLD transfer.

The considerations:

-

Some brokers charge a buyer-side fee for premium service, so confirm the fee structure upfront.

-

Some earn small referral fees from related services such as valuation or insurance providers, typically AED 200 to 500, which is standard practice but worth asking about for full transparency.

Why rates vary even for the same property

A common misconception is that the rate is fixed by the property. It is not. The same buyer can receive different offers from different banks, and understanding why is central to choosing your route.

-

Each bank follows its own risk-assessment model, so differences in cost of funds, credit policies, and lending appetite cause rate variations even for the same property.

-

Headline rates are typically reserved for high-income applicants with low LTV ratios and salary-transfer commitments, while self-employed and non-salary-transfer borrowers should expect 0.20 to 0.40% higher.

-

Most UAE mortgage rates in 2026 fall within roughly 3.9 to 5.5%, depending on the lender and borrower profile.

This is precisely where broker access proves its value: one applicant, many lenders, and the leverage to find the bank whose appetite best matches your profile this quarter.

A simple way to decide

There is no universally correct answer. The right route depends on your profile and priorities.

-

Go direct if: you have an existing banking relationship with a strong rate offer and are comfortable handling the process yourself.

-

Use a broker if: you are a first-time buyer, have complex income such as self-employment or foreign earnings, or are a non-resident.

-

Do both as research: model your numbers independently before committing. A home mortgage calculator UAE tool lets you estimate monthly payments under different rates, and a home mortgage rate calculator helps you benchmark offers before you ever sign.

The smartest buyers treat the decision as a comparison, not a default. They run their own numbers, understand their profile, and then let an expert pressure-test the market on their behalf.

Where Houzzhunt Mortgage Comes In

At Houzzhunt Mortgage, our role is to give you the access, the pricing leverage, and the clarity that the direct route simply cannot.

As one of the mortgage brokers in the UAE built around the buyer rather than any single lender, we work across the market to find the bank whose appetite genuinely fits your profile, not just the one you happen to bank with.

Here is how we help:

-

Whole-of-market comparison, presenting offers from across leading UAE banks so you see your real options side by side, not a single quote.

-

Sharper pricing in practice, using lender relationships and negotiation to secure terms stronger than most applicants reach alone.

-

Specialist handling for complex files, whether you are self-employed, earning foreign income, or buying as a non-resident.

-

Fast pre-approval, giving you a cash-buyer edge and the confidence to negotiate from strength.

-

End-to-end management, from application and documentation through valuation and DLD coordination, so the process never eats your time.

Choosing between a broker and a bank should not be guesswork. With the right partner, it becomes a clear, informed decision in your favour.

That is the difference Houzzhunt Mortgage is built to deliver. Talk to us before you choose your lender, not after.

Note on figures: mortgage rates, commission ranges, and lending criteria reflect early-to-mid 2026 UAE market conditions and vary by bank, property value, and borrower profile. Always confirm current terms with your advisor before transacting.

Ready to explore your mortgage options?

Talk to a Houzzhunt mortgage expert — free, no obligation.

Apply Now →